Agency Valuations – The Truth About EBITDA Multiples

Recent Posts

I’ve come across a few articles posted by agency valuation consultants challenging the use of EBITDA multiples in valuations. It can be argued that EBITDA is not a measure of true cash flow. It can be argued that such a valuation method ignores intrinsic factors of an agency.

Here’s the problem with those arguments: Buyers and their financiers talk about EBITDA multiples and, when you’re trying to understand the market value of your insurance agency, those are the only two groups that matter.

Key Takeaways

- The market value of an insurance agency is driven by the marketplace of buyers and their financiers.

- Pro Forma EBITDA ≠ owner’s discretionary earnings.

- EBITDA margin and organic growth rate impact an agency’s value.

- EBITDA multiples scale with size.

- Achieving a top-of-the-market multiple today requires a go-to-market strategy.

What is EBITDA and How is it Calculated?

For large businesses, EBITDA is generally defined as the acronym describes: Earnings Before Interest, (Income) Taxes, Depreciation and Amortization. Usually, larger agencies have clean financials, and the owners are drawing market-rate compensation, so there tends not to be very much fluff flowing through the income statement.

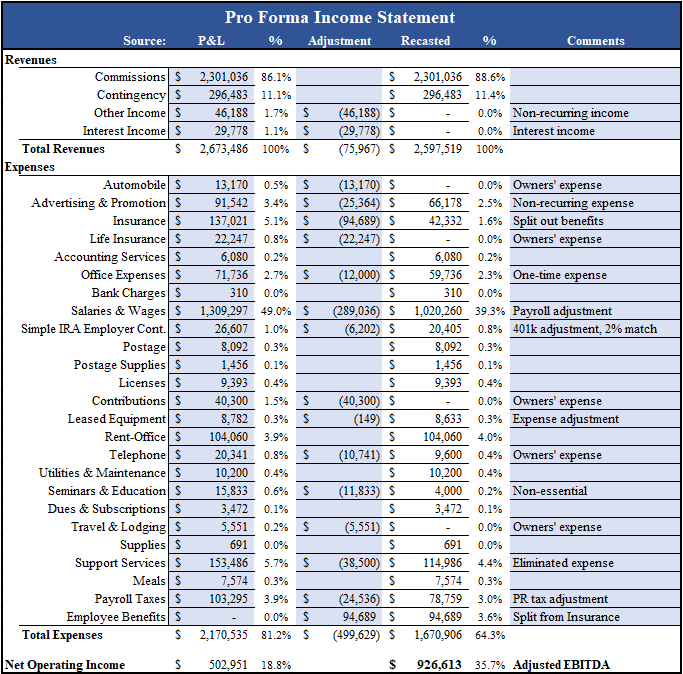

For small to mid-sized agencies though, particularly those with a single owner, the EBITDA calculation involves more analysis and is what we call an “adjusted EBITDA” because there are typically a number of adjustments to remove the owner’s personal expenses. We like to call this “undoing the owner’s tax strategy” and, on occasion, the tax strategy can be pretty extensive. The analysis could look like the following:

It is important to note that the owner’s discretionary earnings are NOT the same as EBITDA. This is often a point of misunderstanding and disagreement between agency owners and buyers. I’ve even seen valuations from certified appraisers that pair the wrong earnings and earnings multiple (e.g. using an EBITDA multiple on DE or P/E multiple on EBITDA).

The goal is to project the buyer’s pre-debt, pre-tax earnings after paying all expenses including the cost of replacing or retaining the owner. The replacement cost could be equivalent to a manager’s salary, a percentage of the owner’s book of business if they need to transfer accounts to a producer, or a combination of both, depending on what the owner(s) do in the agency.

Further to the point, when dealing with a specific buyer, the EBITDA calculation becomes a “pro forma EBITDA”. Most likely, the buyer is not going to show you their synergies, which can be revenue enhancement from better carrier contracts or expense reductions due to job redundancy. Many larger buyers however will want to cushion the EBITDA with corporate overhead expenses, usually a few percentage points on revenue, will need to increase employee compensation to match their corporate level and will add a compensation package for the owner(s) to keep them on-board for a negotiated period. The end result is a pro forma EBITDA number that can be much less than the owner’s calculation, possibly by 10-30%.

What is a Normal EBITDA Margin?

The average agency pro forma (adjusted) EBITDA margin is 35% of revenue. It has been a mystery to me how such a uniform industry can have similar businesses operating at significantly different levels of profitability. It happens though. Some agencies operate at 50+% EBITDA margin (it’s true), and others are barely breaking even (also true).

I discussed Insurance Agency Financial Models in another post. The key for you to understand is that buyers expect a pro forma EBITDA margin of around 35% when valuing an agency on a multiple of EBITDA. For large firms, that’s a sustainable margin.

When acquiring an agency as an operating business, buyers want to ensure the business will grow in the future. Therefore, it’s hard to convince a buyer that they can cut all sorts of expenses post-transaction if the agency hasn’t been operating as lean as you are proposing. If you want to get credit for a higher EBITDA margin, then prove it out by running lean for a year or two before selling the agency.

Based on my experience, high margin agencies, those having EBITDA margins over 45%, fall into three categories:

- Producer-owner led: The owner is the rainmaker, eliminating a producer commission expense. Revenues tend to be under $1.5M, but the profit margin to the owner can exceed 70%.

- Acquisitive: Agencies scaling through tuck-in acquisitions. The margin is artificially high because an organic growth engine is absent.

- Niche, marketing-driven: Not true for every niche agency but, in this model, the agency drives leads and CSRs write the business. Because the agency deals in one type of business, processes are efficient and retention is higher.

Out of the 3 models above, only the 3rd one has an arguably sustainable margin and those types of agencies are rare. To achieve a market value EBITDA multiple on a higher-than-average EBITDA margin, you will have to justify it by demonstrating that organic growth, not just retention, is sustainable long-term.

Why Value on EBITDA Multiples?

First, recognize that cash flow matters. Your agency’s earnings affect a buyer’s ability to pay debt service on the acquisition. Two otherwise equal agencies with different EBITDA margins are not of the same value. Since EBITDA represents a go-forward, pre-tax, pre-debt service cash flow, it also functions as a measure of return on investment (the ROI = 1/EBITDA Multiple).

Second, large firms are valued on EBITDA multiples, which ultimately drives the standard. EBITDA is the standard earnings benchmark because it’s also an easy one to calculate and provides a path to normalizing expenses, as discussed above.

What are the EBITDA Multiples in Today’s Market?

The multiple of EBITDA a buyer is willing to pay is driven by several factors, including:

- The availability of other relatively similar agencies.

- The perceived risk of the revenue and earnings, which has different components unto itself.

- The cost and availability of capital, affected by interest rates.

- The potential synergies, which will be unique to specific buyers.

- The value, as a multiple of EBITDA, of the acquiring firm.

The market value of an agency as a function of pro forma EBITDA multiple is a sliding scale that increases with the size of the agency. Historically, valuations for preferred P&C and benefits firms were roughly:

- Small agency (under $1M revenue): 4-6 x pro forma EBITDA

- Mid-sized agency ($1M-$5M revenue): 6-8 x pro forma EBITDA

- Larger agency ($5M+ revenue): 8-10 x pro forma EBITDA

Today, the key difference in the market value of agencies lies in the number of capital-backed buyers (private equity-backed and publicly traded), which has increased 10-fold in the last decade. Due to their capital structure, growth strategy, and intrinsic valuation, capital-backed firms are paying 20-50+% higher multiples than the historic averages.

Example: Mid-sized agencies, the group that saw the highest valuation lift, are valued at ~ 7.5 to 12 x EBITDA in today’s market.

Achieving those type of valuation multiples in 2026 is not a given though.

Capital-backed buyers are feeling the pressure of higher interest rates post-2021, inflation, and softening P&C premiums. Because of these factors, buyers are scrutinizing deals harder than ever on strategic fit, organic growth rate, and a seller’s transaction objectives and offers regularly include an equity rollover component to align the seller with the buyer longer term. Clever buyers are also manipulating offers to present headline multiples that are not achievable but are designed to lure sellers into a trap, which I wrote about in my article The Tantalizing Trap of 30 x EBITDA Offers.

As is the case in any market, working with an experienced M&A advisor that is active in the marketplace is key to maximizing your ability to find the best buyer for your agency and to minimize your risk of making a bad deal.

The Bottom Line

Valuing an insurance agency on a multiple of pro forma EBITDA is a valid approach because nearly every buyer uses it. It is important for agency sellers to understand how EBITDA is calculated, which may include adjustments that you disagree with. The pro forma EBITDA margin should support long-term stability of the agency so you need to consider the balance of growth and profit.

Achieving a high valuation multiple is not as easy today (2026) as it was in prior years (e.g. 2020-2022). The combination of higher interest rates, a softening P&C market, and the emergence of AI is putting increased pressure on acquirers. As a result, the spread between a top-of-market valuation and an average one increasingly comes down to how well an agency is positioned and marketed, which is precisely where an experienced M&A intermediary earns their keep, dressing an agency up for market and presenting it to the best pool of strategic buyers.

Posted by: Michael Mensch, Founder and CEO

Direct: (321) 255-1309

Schedule a meeting with me if you want to talk about your agency: Mike’s Calendar

Experts in Insurance Distribution Business Valuation, Sale, and Acquisition

We deliver superior results through our industry expertise, transaction expertise, and professional network.

Contact us